1 min read

ICBA ECONOMICS: Household Formation, Immigration and Housing Markets

By Jock Finlayson, ICBA Chief Economist The 2024 federal budget unveiled dozens of new initiatives intended to address Canada’s unfolding housing...

2 min read

Spending by households on goods, services and housing represents more than three-fifths of all economic activity in Canada. Households finance their consumption through employment earnings, cash transfers received from governments (e.g., EI benefits, OAS payments), and other sources of income (e.g., interest, dividends, capital gains, pensions, and rental income). For a typical household, whatever income remains after all of its consumption expenditures are made is channeled into savings vehicles (bank accounts, RRSPs, RESPs, TFSAs, etc.) or invested other types of assets (e.g., stocks and bonds, real estate and private businesses).

Statistics Canada collects information on the sources and amounts of annual household income as well as on the patterns of household spending on goods and services. In this post, I summarize the most recent Canadian data and comment on household income and spending in B.C. and Alberta.

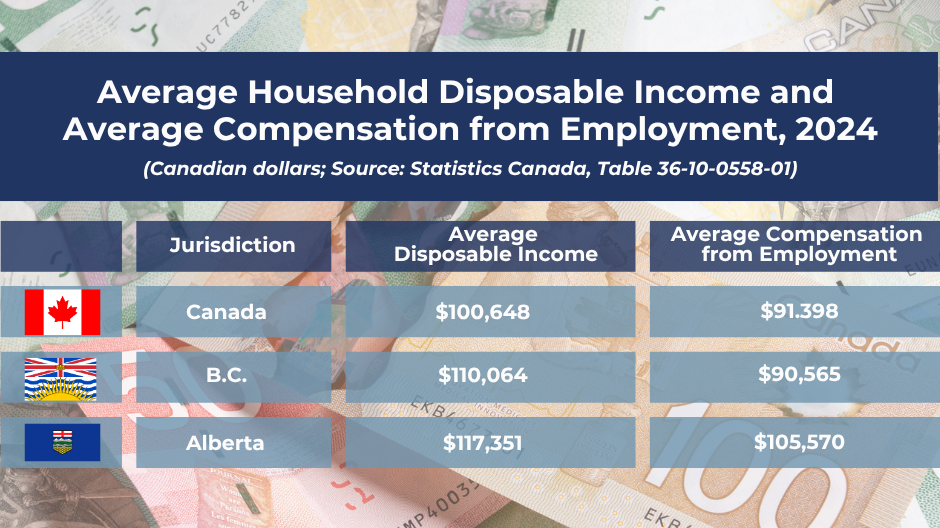

Figure 1 summarizes the average value of household income in 2024 – nationally, and in both B.C. and Alberta. The two westernmost provinces lead the country in average household disposable income, with Alberta enjoying a hefty 17% advantage over the national benchmark.

Figure 1

Disposable income is calculated after deducting direct taxes paid, but it includes transfers from governments. By far the biggest slice of household income is earnings from employment. In 2024, Alberta led the country in employment income per household at $105,570, comfortably ahead of Canada ($91,398) and B.C. ($90,565). B.C. also trails well behind Ontario ($99,962) on this measure.

Alberta’s impressive performance on employment earnings reflects both its generally robust economy and the size of the energy sector. Oil and gas ranks as the highest-paying industry sector in Canada. Adding jobs in relatively high-paying industries like oil and gas, pipelines, utilities, mining, and professional and scientific services is an important way to lift average household incomes. In contrast, adding jobs in relatively low-paying industries has a smaller (albeit still positive) impact on household income.

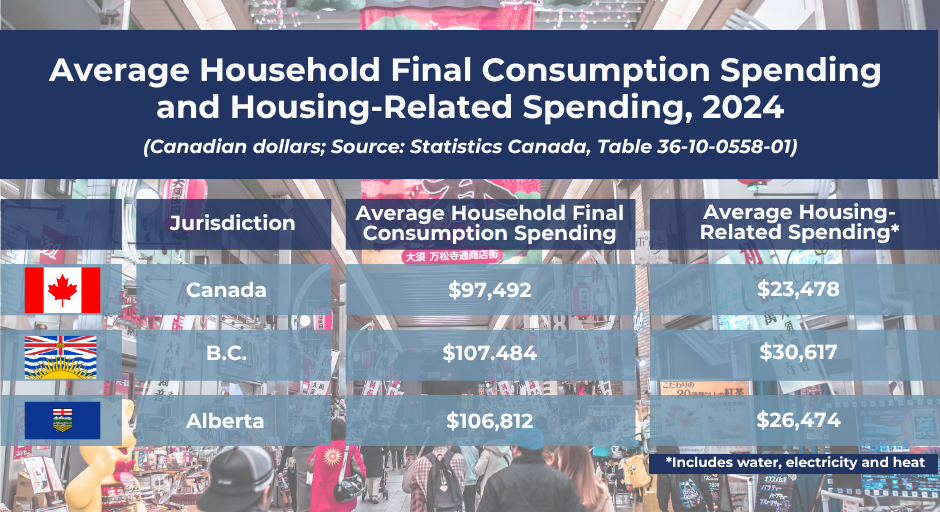

Figure 2 reports data on household final consumption expenditures in 2024 – again, for Canada, B.C. and Alberta. Intriguingly, while Alberta leads the country in disposable income, B.C stands first in average household spending on goods, services and housing combined, at $107,484 last year, roughly $10,000 above the national amount.

Figure 2

The principal reason why the typical B.C. household spends more than its counterparts in other provinces is that housing-related costs are higher on Canada’s west coast – reaching $30,617 for the average household in 2024, versus just $23,478 nationally. If the latter two figures strike readers as low given endless media stories decrying high steep housing prices and rents in many parts of the country, that’s mainly because a large fraction of Canadian homeowners carry only small mortgages on their principal residences or else own these properties outright.

Nationally, housing is the largest expenditure category for most households, followed by transportation (which includes deprecation costs for households that operate vehicles) and food produced and consumed at home. The ranking of the various spending categories is similar across the provinces.

The flip side of high household final expenditures in B.C. is that residents have less capacity to save money out of their total disposable incomes. This is shown in Figure 3, with B.C. emerging as a “low-saving” jurisdiction compared to Alberta and Canada as a whole. It should be noted that the numbers reported in Figure 3 do not include changes in pension entitlements or in the value of pension-related accounts.

Figure 3

From an economic policy perspective, governments need to understand that a strong, vibrant private sector is the key to growing household incomes in a sustainable way and to increasing the real spending power of Canadian consumers. An ever-expanding and more costly public sector will not deliver sustainable improvements in household incomes or long-term living standards.

1 min read

By Jock Finlayson, ICBA Chief Economist The 2024 federal budget unveiled dozens of new initiatives intended to address Canada’s unfolding housing...

1 min read

By Jock Finlayson, ICBA Chief Economist Preliminary estimates from Statistics Canada show that B.C.’s economy grew by a modest 1.6% after inflation...

1 min read

By Jock Finlayson, ICBA Chief Economist Canada is sitting on $7.4 trillion worth of fixed assets, yet we’re still grappling with a housing crisis and...