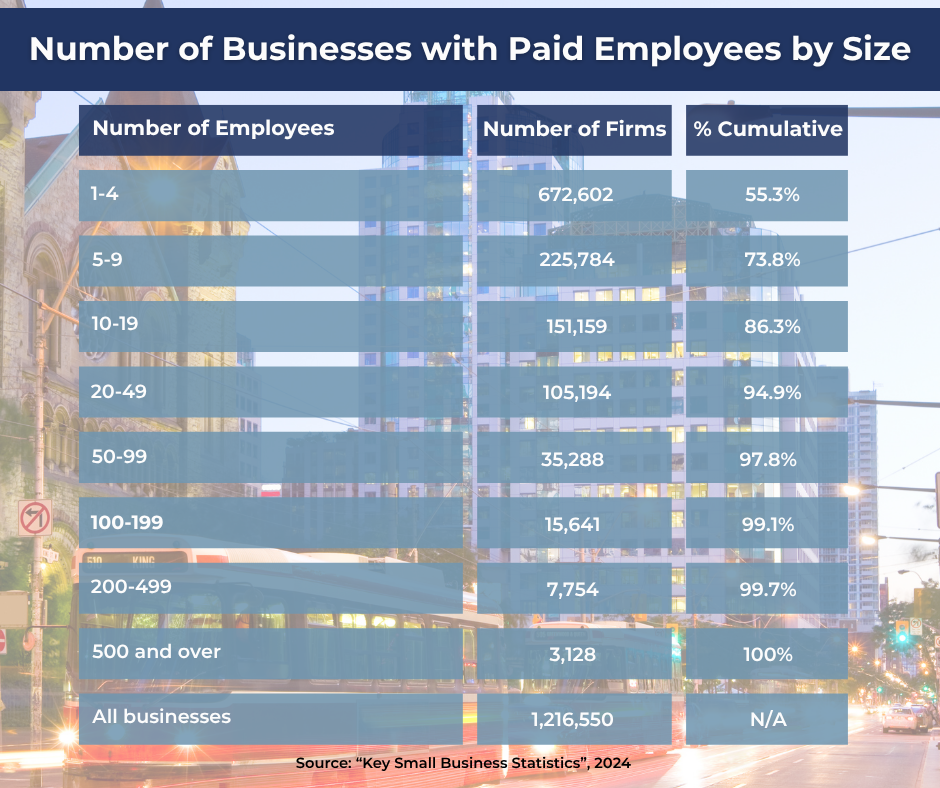

Canada is known as a jurisdiction where small and medium-sized enterprises (SMEs) are ubiquitous – found on every commercial street, every community, and every sector of the economy. By 2023, Canada was home to 1.22 million SMEs – defined as firms with between 1 and 499 paid employees. This definition excludes self-employed individuals who do not have other workers on the payroll.

Within the overall SME category, businesses with fewer than 100 paid employees are commonly classified as “small,” while mid-sized companies are those with 100 and 499 employees on the payroll. In 2023, 97.8% of all registered businesses in Canada were considered small and another 1.9% fell into the medium-sized grouping. In the same year, only 0.3% of all Canadian enterprises were deemed to be “large” – based on having 500 or more employees.

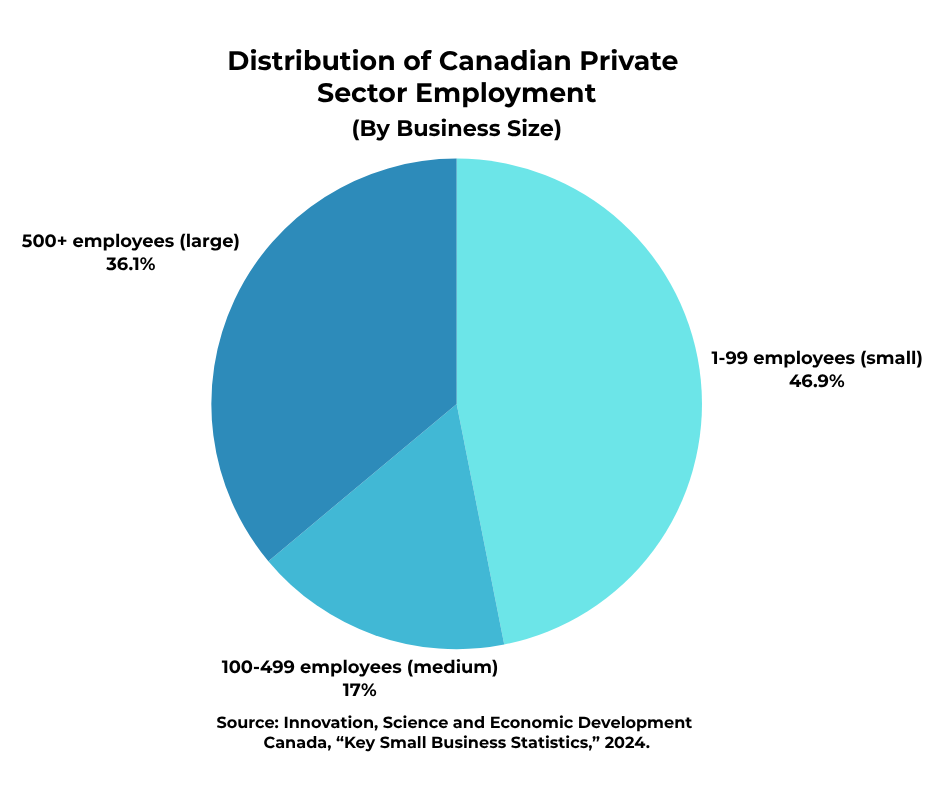

SMEs account for the bulk of Canada’s private sector workforce (64% of total private sector employment in 2023). As for their contribution to economic output (GDP), SMEs’ share has averaged about 50% over the last several years. SMEs also supply about 40% of Canada’s goods exports – an impressive showing.

Figure 1 provides summary data on Canadian SMEs and their role in the wider economy. Figure 2 shows the distribution of private sector payroll jobs by business size.

The distribution of SMEs across the economy is not uniform. Some industries are more oriented toward smaller firms than others. The differences aren’t great, but there is some variation.

Construction stands out as a sector that is particularly SME-friendly: added together, small and medium-sized firms comprise almost the entire population of Canadian construction companies. Remarkably, just 0.1% of the 153,000 construction businesses counted by the federal government in 2023 had more than 500 paid employees.

One marker of an open, thriving economy is a healthy rate of business formation. New business entrants are a vital source of dynamism and innovation in most industries. They also help to inject competitive pep into the wider economy – something that’s badly needed in Canada, given the cartelization of swathes of our economy. Building an overall economic environment that encourages the establishment and growth of new firms should be a top priority for governments at all levels. Unfortunately, Canada has seen a slowdown in the pace of business formation in the last decade or so, with the number of new firms barely replacing those that disappear in some years. This trend should be of concern to policymakers. Put simply, more effort needs to be directed to improving the climate for start-ups.

For entrepreneurs and others who invest in start-up and early-stage businesses, the risk of failure is ever-present. The Canadian data confirm that many new businesses don’t survive. In the goods-producing sector of the economy (which includes construction), about 70% of new businesses survive for at least five years; in the broad services-producing sector, the five-year survival rate is lower – 56%. Ten-year survival rates are around half in goods-producing industries and just 35% in service industries. This underscores the fact that starting a business is a risky endeavour.

Finally, we briefly consider the number and impact of “high-growth” businesses – defined as the sub-set of SMEs that report well above-average increases in employment, revenues or both over three- and five-year periods. As documented in a 2017 study, high-growth Canadian companies were responsible for more than two-fifths of net private sector job growth in the early 2010s. High-growth businesses exist in every major industry – they are not concentrated in the “high tech” sector – which tends to garner disproportionate attention from the media and many politicians. Indeed, measured by increases in revenues, construction was near the top among all Canadian industries in the share of high-growth companies during the half decade leading up to the COVID-19 pandemic.

{kind=link}

{kind=link}